I am just home from an excellent technical summit put on by @Cybera. It was the @CyberSummit14.

At this summit, I gave a talk on "FTTH as Municipal IaaS". I started my session reliving the success and failures in the Canadian FTTH market. Adding the failures part made the session way too long, but it set the light on the reality of Canadian FTTH; it is very complicated, fraught with active enemies, and has poor results when outside of a bigger-picture initiative.

In general, to summarize in one sentence, is that citizens don't generally volunteer to be customers of government, and municipalities shouldn't be involved in the retail ISP/TV/Phone provider industry.

The reasons are many and varied in their depth, and I'd be glad to elaborate on-demand for anyone, but fundamentally, the initiative of Municipal FTTH will likely only succeed when part of a much larger initiative. And the larger the capital costs, the more risk, and thus the more mitigation, and rightly so the more options of value-chains are required.

Such as, if the municipality is larger than 400K dwellings, its value-chains may look as follows:

- they likely have 3000 - 5000 things that could be points-of-interface within their corporate boundaries that will at some point in the very near future need a high-speed data connection.

- they're likely to have 5000 - 15000 municipal partners (schools, police, fire, airports) that would immediately see value in connecting to a municipality-wide high-speed network.

- there is likely 50k or so SMB's and enterprises that could find ways to be more profitable within the community by being better served and more connected throughout the community.

- and the 400K dwellings would all be near one of the points above and would likely want competition in the market for both innovation and opportunity in the digital economy, and that the muni would like to exercise their diminishing opportunity to reach those dwellings in the existing, but finite, right-of-ways.

It makes sense to mitigate the risk of the wants with the needs, and cost of the needs with the wants, and to roll out a city-wide solution that empowers all levels of public interest. But it doesn't make sense for that municipality to venture into the private-industry layer of retail services to those businesses and homes, or possibly even those civic partners.

The conflict-of-interest is in the purpose of a municipality and the purpose of retail services, which, of the former I believe is fundamentally and necessarily open within its governance, and of the latter, exclusionary when looked at on the boundaries of its marketing.

A municipality's purpose is not focused on a specific target-market within its jurisdiction, it is about all of the citizens, all of the time, and validation is predicated on the perception of opportunity to lifestyle afforded, to the citizens, by the political and administrative platform in office.

A for-profit business, in the best possible situation, is focused on their customers' happiness, which is validated with profit.

The dichotomy is that the governance, sustainability, and capital cycles operate on and in polar-opposite paradigms. Mixing the two will never be a solution, but rather a push-pull relationship with completely different market drivers; one being political pressures, the other private-market pressures. In a worst-case scenario, it will be a lobbying and unfair advantage relationship that can only end in scandal.

“Most people don’t volunteer to pay the gov’t for anything...”

Is there really a place for Municipal FTTH, if municipal-purpose is really founded on the affording of jurisdiction-wide opportunity, but not on validation by profit? And if there is, is there a way for that municipality to avoid the conflicting interests of the complex layers of execution required in the full-stack of a FTTH network, operations, and retail services?

YES, and yes.

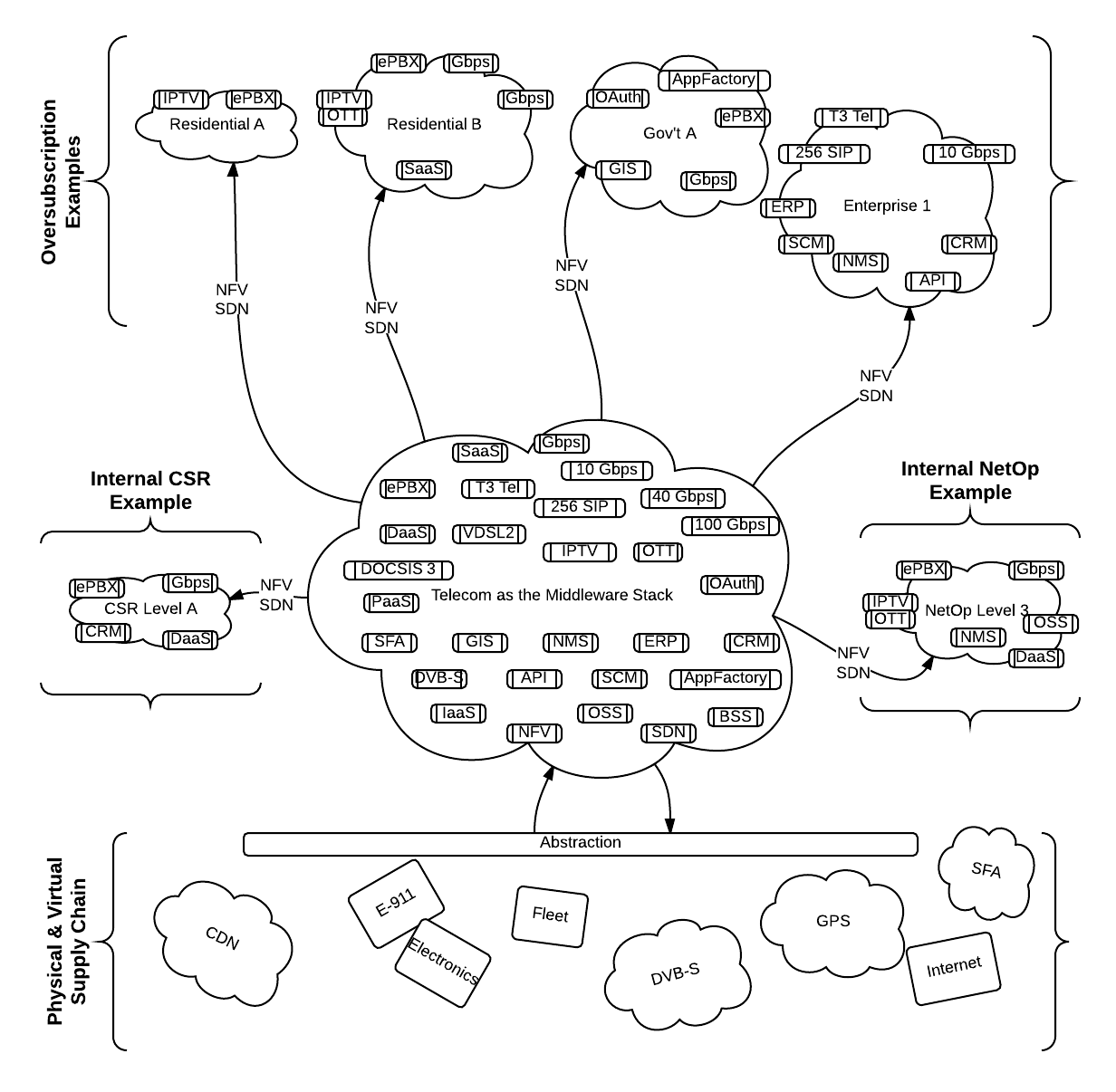

The larger municipalities would be well served to participate on the layer that it knows best, which is infrastructure. I say "knows best" in context to the complexity of services delivered within the most retail-customer-facing side. It is similar to the complexity of the services and upshots of roads, but dissimilar to the relative simplicity of electricity and water upshots at the retail demarcation point.

That FTTH infrastructure layer, which would provide opportunity across all four municipal value-chains mentioned above, is also mitigated by the full deployment having many more possibilities of value realization, than proportionate deployment based on priorities or demands of only one or two value-chains. A full commitment to a full FTTeverything deployment is a set-it-and-forget-it for 40-60 years solution. Not one that is only an immediate bandage, nor one that is overkill, but rather a finite policy on connectedness being as basic a citizen need as clean water, sewer, garbage pickup, roads, electricity, and bylaws.

In my opinion, the Municipal FTTH space must demarcate as the fibre asset in the ground up to the premises edge termination point. This layer boundary is referred to as the NetCo. There is a possibility to extend the NetCo mandate through the other layers (OpCo and NetCo) with a soft demarcation point within each premises, providing basic internet at the minimum standards set federally within its definition of "highspeed" with zero bells and whistles. The latter half is not a contradiction, it is a base-level service for a jurisdiction-wide option of opportunity, but also a possible key change-agent. Contact Lightcore Group for complete details on the deployment and risks analysis in your municipality, today.

Beyond the NetCo is the network operator that manages and enforces policy on the network to the Retail Service Providers (RSPs). There is no consideration for net-neutrality here other than that non-neutral is a business model, and I fundamentally believe that private-industry business-models should not be regulated, but rather that if there is fundamental belief in net-neutrality business-models than government may need to look at ways of incentivizing private-industry to grow in that direction, organically or naturally. The same way that solar, wind, and bio-fuel energy-sources required heavy subsidization (development capital, grants, and otherwise) to become available in the market as an option, so too might net-neutrality-based business-models need subsidizing, not unfair advantage, upfront.

There needs to be clear delineation between the one or more RSP's and the NetCo, and that is the role of the OpCo(s). The OpCo(s) is a gateway and gatekeeper for RSP's to on-board and compete openly, without the ability of the RSP to influence the municipality with direct-lobbying channels, unfair contracting-mishaps, or unfavourable connection between "government program" and "retail services". The OpCo(s) has been suggested by some to be a good fit for a non-profit. I fundamentally disagree. Simply because the purpose of the OpCo(s) is to entice as much competition as possible without the politics, turn-over, or personal-passions getting in the way.

In an ideal world, the OpCo(s) would be robots, or fixed-fee 5-year tendered contracts for up to [the maximum connections to each single premises, minus one] wholesale management companies (which of course would be a mix of interest groups, incumbent subsidiaries, and market entrants), but a mix of interest options would make sense.

On the Retail Service Provider layer, it is very complex, full of regulatory oversight, and content-owner control. Each retail provider should be able to choose its OpCo at will, in this model, in the hopes of driving up innovation, collaboration, and not collusion between the OpCo(s).

What about the smaller communities? Is there something that they could do even affordable?

YES, and kind-of.

In a smaller market than 100K, and looking at a new FTTH initiative, as laid out above, is not going to work very well. Functionally, it can be deployed without issue, but that "technical feasibility" is only 20% of the whole picture.

When Lightcore Group looks at feasibility, we break it down into five distinct categories, and then build them back up inter-vetted and intertwined into a solid statement of feasibility.

In short summary, our municipal FTTH feasibility method is acronym'ed S.T.E.L.E.

- Social Feasibility

- Technical Feasibility

- Economic Feasibility

- Legal Feasibility; and

- Environmental Feasibility

The truth is that launching an ISP in any municipality of any size is generally going to be facing a large uphill battle against bundled services from other providers.

If you're considering an under-served or un-served market, then none of this applies to you; call Lightcore Group, we can have you up and running successfully, the quickest.

That bundling is purposeful. It makes the existing services sticky to their provider. We realized in the O-NET launch, rather quickly, that you at least need to bundle some sort of IPTV content with your service to entice people to consider changing their life habits. But that is just it, you're asking people to change their universe for you. No amount of community engagement is going to get people to make the purchase to the tune of 40%+ take-rate on day one, or year one, unless you have some other major change-agent, such as a fanatically-loved brand like Google Fiber. Or if an incumbent plays on your network (again this is not an under-served or un-served market we're talking about), which they won't without market pressure to do so, you'd have a better chance of switching people to your FTTH infrastructure without them even really knowing via a "standard or special" network maintenance initiative to pair the two.

A small community may be able to solicit a competitive carrier to become a market entrant, but the numbers have to be there for their value to initial marketing and on-boarding costs to balance. But regardless of RSP's, if they aren't fundamentally different in the customer-perception of their vision and mission (meaning don't sell "copper, me too" bundles and packages over FTTH, which is as helpful as "press or say one"), then the RSP's will need to wait-out existing contracts, brand development/trust, and significant losses somewhere in the overall FTTH initiative, which regardless will be borne by the citizen. And don't be shy in your estimates of ruthless competitive pressures by existing carriers not in favour of given market share away.

My recommendation is NOT that smaller communities avoid FTTH, which some people may have mistaken me for saying tonight, but rather that their initiative has to be about a bigger picture, a longer time-frame, and ultimately a multi-municipality collaborative (meaning shared governance) effort to culminate a large enough market to entice positive industry change, and relevant local rewards of that change. Smaller muni's need to work together to create a larger collective market that is accessible "as a service" to the remaining layers needed to generate the opportunity demanded of their jurisdictions.

We would welcome any municipality considering a FTTH initiative to give us a call to get our perspective of the realities of the industry without either the hyperbole nor FUD (fear, uncertainty, and doubt), of both camps on either side of our positioning.

Our model for smaller municipalities is based on risk mitigation the open practices and reference model operations that get a muni up and running quickly. Our Municipal FTTH funding division, Lightcore Finance, will fund nearly any FTTH project that has been vetted bout our team of industry experts to ensure valid practices and procedures are being proposed and adhered to.

If you have a question, post it, I'll answer it. :)